1 - 2 - 3 - 4 - 5 - 6 - 7 - 8 - 9 - FAQ - Top Annuity Lies

Index Annuities - Immediate Annuities

Deceptive arguments from insurance salesmen:

1) Q. "Lots of people are happy with annuities."

A. Annuitants are happily ignorant and/or confused. Because of the opacity of the fees, and the complexity of the return calculations this makes it impossible for investors to figure out if they’re getting a good deal or not (source). Most investors don't know the difference between interest payment rate and return on investment. All too often it isn't until they pull their money out that they figure out what they got into, although most never have a clue what their return on investment was and how they would have done had they otherwise invested in a bond heavy portfolio. Sometimes investors are constantly adding to an annuity, making it even more difficult to calculate ROI.

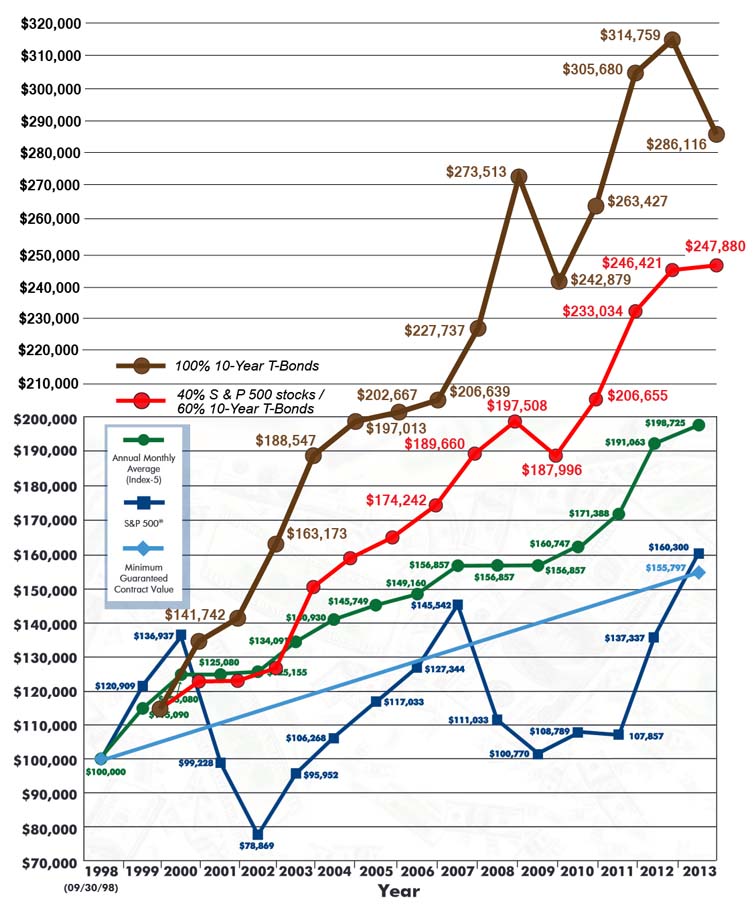

Investors are usually completely unaware of all of the negatives described on this site because the agent who sold them the annuity conveniently never told them. Typically they are completely unaware that they have been sacrificing returns that they could have otherwise been earning with a low-risk portfolio of bond/stock ETF's, or even CD's, including during the "lost decade"! Calculating annuity returns is so complex that consumers can't understand what's really happening. Fees and costs are also hidden. Most annuitants don't know the difference between annual return and return on investment (ROI), and the fact that they will NEVER get that advertised rate of return as long as they live. According to Craig J. McCann, Ph.D., CFA of the Securities Litigation & Consulting Group, Equity indexed annuities are so complex that the true cost of the product is completely hidden. Would they be happy if they saw this chart?

{kind=link}

2) Q. "I agree that variable annuities are terrible investments but ____ annuities are different."

A. This is how insurance agents pretend to have boundaries and then hopefully be trusted. If they bad mouth variable annuities then maybe you'll fall for one of their other high-commission products. There's been a lot of bad press about variable annuities but maybe you haven't been paying attention to the bad news about fixed and index annuities. The insurance industry is always trying to create another inferior financial product under a new name. If you notice, their sales pitch is always big on empty talk and cheer leading, but devoid of facts and data that would support their argument that the new annuity product is somehow better than a traditional diversification of bond and stock ETF’s.

3) Q. "Fixed annuities provide guaranteed income for life."

A. This is the happy cover story lie. In reality a fixed annuity provides a very low return on investment. The advertised "guaranteed" annual rate of return is the distraction while they systematically widdle away at your principal so that by the time you die or need to cash out of the annuity, it has been seriously eroded or dropped to zero. And that "guarantee" is only as strong as the one single insurance company that makes the guarantee. A fixed annuity also cannot be strategically rebalanced as a bond / stock ETF portfolio can, annuity payments are taxed at a higher rate, etc. It is true that a 60 / 40 bond portfolio is not guaranteed, but nobody needed such a guarantee when even during the so-called "lost decade" this 60 / 40 portfolio gained 5.6% per year and at no point was ever in danger of failing to continue to grow. From 1999 - 2013 a low-risk 25/75 portfolio provided a 5.5% return on investment (ROI) when rebalanced at the end of each year.

4) Q. "I am selling an index annuity that pays 6 1/2% per year in lifetime guaranteed income regardless of what happens in the stock market"

A. That's interest rate -- Not return on investment (ROI)! The actual ROI with these annuities is never the advertised rate that you are touting! If the annuitant lives 20 years then their actual ROI would be about 1.5% -- not 6.5%. This is because those 6.5% payments are subtracted from the death benefit value on the contract, along with additional 3 - 4% annual fees.

If the annuitant lives 30 years then their actual ROI would be 3.2%. These annuities typically have extraordinarily high fees of 3 - 4% which erode the actual cash surrender (or death benefit) value of the annuity. An age appropriate mix of bond and stock ETF's would be a vastly better choice. Ask yourself, in 10 or 15 years will interest rates be above 3%? With history as our guide I would guess yes. With history as our guide will a portfolio of 28% S&P 500 index / 72% total bond market index do better than 3%? With history as our guide I would say easily!

{kind=link}

5) Q. “I have met people who had to go back to work because they suffered great losses of their retirement money on Wall Street."

A. They had to go back to work, not because they didn’t put their money in an annuity, but because they took too much risk for their age by putting all or too much of their money in stocks. They were not properly diversified (in stocks and bonds) in accordance with their age and tolerance for risk. Even while taking out 5.5% per year, from 2000 to 2014 a 60 / 40 portfolio never lost money. As you get older you generally favor bonds more and more. If you have already reached the financial "finish line" then sitting on more and more cash may be appropriate for some investors.

6) Q. "Annuities are an asset class just like any other investment."

A. So what?! Futures are an asset class. Stock Options are an asset class. Loans like promissory notes are an asset class. But you wouldn’t want to touch any of them. Just because insurance products are classified as an asset class doesn’t make them a bread & butter part of anyone's portfolio. It’s an attempt by Mr Annuity Salesman to make you feel warm and fuzzy about it.

7) Q. “There are many bad insurance agents out there, but I am not one of them."

A. But you’re still selling commission-based annuities to your clients!!! A conflict of interest exists. If you sell your clients anything other than low cost, penalty-free Vanguard annuities then that is proof positive that it’s the commissions that are motivating you -- not the product itself.

8) Q. "I am a fiduciary and I recommend annuities, therefore they are good investments."

A. Then 1) You're certainly not a fee-only fiduciary and 2) You are a prime example of how an adviser can "double dip" if they are merely a fee-based adviser and a prime example of why an investor should seek a fee-only registered investment adviser and for a one-time consultation if they can't figure out how to do it themselves. The potential for conflict of interest and bad advice still exists when working with a fee-BASED adviser.

9) Q. "I had a client complaining about how they were getting a pathetic 0.15% return from a certificate of deposit. Why wouldn’t they invest in an index annuity instead because an index annuity easily pays much better return?"

A. First of all, an index annuity carries more risk than a bank CD. Secondly, putting money in a CD is not investing in today's low rate environment, assuming that financially the client has not “reached the finish line” so to speak. Comparing a financial product to a CD is like comparing your quarterback to JaMarcus Russell or Ryan Leaf. How about comparing an annuity to a balanced allocation of bond and stock ETF's!

10) Q. "Comparing annuities to a CD is a valid comparison. The majority of annuities are purchased by seniors who are doing exactly that."

A. Putting “investment money” in a CD is not investing. "CD investors" are typically totally ignorant of how bonds protect against stock volatility. The Boglehead philosophy is to never bear too much or too little risk. A CD bares too little risk. A diversified portfolio of bond and stock ETF’s is the solution. For about the same amount of risk, one can achieve a much better return with bond and stock ETF’s. This has been repeatedly proven through independent studies including during the "lost decade" from 2000 - 2009.

11) Q. "Indexed annuities have consistently outperformed fixed annuities and CDs, which they are intended to be compared against."

A. Again, that’s like saying "My quarterback is better than JaMarcus Russell". Nothing to brag about. Try comparing JaMarcus Russell to Tom Brady. Try comparing that index annuity to a diversification of bond and stock ETF’s.

12) Q. "The purpose of an annuity is not to beat the stock market. They should be compared to other insured long-term investments like CD's."

A. Wrong. Again this is like comparing your quarterback to the worst quarterback you can find in order to make your quarterback look good. The "purpose" of investing is to get the best return while assuming a certain level of risk. An annuity should be compared to something of the same risk caliber, and then you pick the best option -- not the worst option. A CD is not investing. The best choice is a very conservative diversification of mostly bond and stock ETF’s, which are 100% liquid, taxed at a lower rate, great for heirs, etc.

Q. REBUTTAL TO THE ABOVE ANSWER: "I disagree. Comparing an annuity to a bond/stock portfolio is like trying to compare a quarterback to a field goal kicker. It's not an apples to apples comparison. They both score points, but they do it in completely different ways."

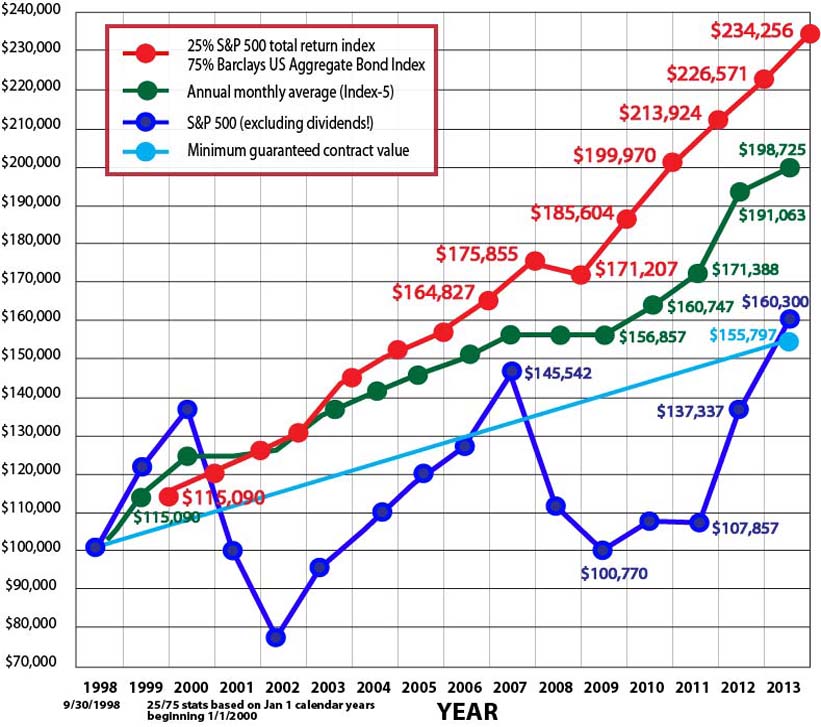

A. You are being deceptive. How they score points is irrelevant. What matters is how many points are scored (return on investment) when considering that both take on very minimal risk (apples to apples). People want the best return for the minimal risk that they are willing to take. When you look at this return chart it is clear that a 75/25 portfolio is not excessively risky at all. It is also clear that the annuity consistently under performs even during this bear market time period.

{kind=link}

13) Q. "Indexed and Fixed Indexed Annuities are NOT investment products."

A. So what! It makes no difference how you want to "classify" annuities. Like any investment, an annuity is a tool to generate income / grow your principal. So are bonds and stocks! Annuities are marketed and sold to very conservative investors who are seeking a place to put their money. They want the best return that they can get for minimal risk. A conservative diversification of stock and bond ETF’s is the low cost, low taxed, time tested best choice.

14) Q. "An asset manager probably costs you just as much as a commission-based adviser."

A. Commission-based "advisers" love to present this false choice argument. In reality both asset managers and commission based "advisers" are bad choices, with the commission-based “adviser" being the worst of the two evils. Fortunately these aren't the only choices at your disposal. That’s why an investor who can't figure out how to do it themselves should hire a fee-only RIA for a ONE-TIME consultation only -- Not a full time consultation! Don’t pay them to constantly “manage” your money year after year.

15) Q. "You failed to consider the cost associated with investing. You will spend a minimum of 1% a year plus fees for an investment adviser."

A. You conveniently assumed that the only alternative is to pay an “asset manager” year after year. That would be almost as bad a choice as locking one’s money up in an annuity. Instead, if they can’t do it themselves (it’s very easy) they should hire a fee-only fiduciary registered investment adviser for a one-time consultation to device a “game plan” and help build a portfolio.

16) Q. "When recommending an index annuity I’m not selling the best returns. I'm selling protection."

A. Returns matter!!! Who are you kidding? You are actually selling missed out on returns! And if you are selling "protection" then you are selling snake oil. At no point in the last 14 years was anyone who put their money in a diversification 60% bonds and 40% stocks in danger of losing principal.

17) Q. "What if someone has kids that cannot manage money responsibly and he wants to provide them with a monthly cash flow after he dies? Don't you think that an annuity would be a good choice for the kids' future?"

A. No! Locking money up for 40 or 50 years in an annuity is certifiably insane! They need a living trust instead. For starters, by the time the kids reach age 59 1/2 the high annuity fees would have wreaked havoc on the account! Actually, if left with an annuity there would be nothing stopping them from cashing out of the annuity (with penalties) anyway. They probably would take some or all of the money out at some point. If and when they did so they would have to pay a devastating 10% IRS penalty plus a separate state tax penalty, plus the higher ordinary income taxes. In short they would need a living trust anyway. With a living trust you can also shield children from things like civil lawsuits and nasty divorce settlements by staggering payments (ex- 1/4 at age 20, 1/4 at age 25, 1/4 at age 30, 1/4 at age 35). By staggering payments this would also protect them from blowing the money (parties, gambling, buying fast cars, etc) as young people are prone to doing.

18) Q. "There is nothing wrong with using fixed annuities and fixed index annuities for the income portion of your portfolio. They are a tool like any other financial instrument. Used properly they can be effective, safe and very good for the client."

A. This is nothing more than an insurance salesman’s happy talk that attempts to make these inferior financial products (annuities) seem like some sort of bread and butter part of a portfolio. There is nothing “wrong” with an annuity as long as you enjoy earning lower returns (as demonstrated by studies), enjoy paying higher taxes, enjoy locking your money in prison under threat of insurance company early withdrawal penalties, enjoy debilitating participation rates and performance caps, enjoy screwing over your heirs, etc!

19) Q. "All financial companies 'profit' off their customers whether there are up front "fees" or commissions paid directly to an agent."

A. There is absolutely no comparison between an ETF and an annuity. No contest. You can invest $100,000 in an ETF for free through Schwab.

20) Q. "When your ETF got COOKED in 2008, then your client had an emergency, they lost 50%. Great plan!"

A. No. Nobody lost 50% if they were properly diversified in a conservative portfolio of bond and stock ETF’s. In fact with a 60 / 40 portfolio they lost less than 1% during this bearish stock market period from 2007 - 2009. During the entire 14 year parody from 2000, the 60 / 40 portfolio beat the index annuity by 24%. On the other hand, with an annuity, if someone had an emergency they were faced with things like contingent deferred sales charge penalties, IRS and state pre-59 1/2 early withdrawal tax penalties, the higher ordinary income tax rate, last in / first out tax treatment, the need for tightly controlled withdrawals, etc, all because money in an annuity is locked in prison long-term. With a separate account of bond and stock ETF's they could take out as much as they needed without any penalties. Furthermore if they had NO emergency then in 2009 they had a great opportunity to rebalance their bond / stock portfolio to favor stocks in advance of the inevitable stock upswing.

By the way the consumer staples index (ticker symbol XLP) alone only went down 33% from it's 2008 high to it's 2009 low. In fact by November of 2009 this index fund was only down 6%. The consumer staples index is the type of conservative stock ETF (along with a bond index or two) that a market fearing senior citizen would invest in. Not 100% in the S&P 500 index!

21) Q. "If fee-only planners truly believed their advice would ensure that nobody ever runs out of their original principal, then they should sign contracts with their clients saying that they'll pay out of their own pockets if their clients' principal goes to zero."

A. The notion that a low-risk portfolio of ETF's is going to lose principal is absurd. According to William Reichenstein, since 1957 there has never even been a 3 year period in which the 85/15 portfolio of T-bills and S&P 500 index stocks has lost money. Never. Over longer time periods the notion of loss of principal becomes even more absurd.

Here's a better proposition: Why don’t insurance salesmen reimburse their clients if and when the annuities they sell them results in a wealth transfer of 15% to 20% to the insurance company and the annuity salesman as it typically does? And why don't insurance salesmen reimburse their clients if and when the client has to pay surrender penalties and tax penalties because they had to withdraw money early, as approximately 25% of annuitants in fact wind up doing? Or reimburse the heirs of the client when they are stuck with paying taxes on gains that occurred during the client's lifetime? Or reimburse the client when the client loses money in the event of an industry wide systemic failure that drains the state guarantee fund?

22) Q. "I am a Certified Financial Planner!!!! Therefore everyone should listen to me."

A. Certifications mean nothing. In determining if an adviser is likely to give 100% unbiased advice, what matters is whether you are a fee-only fiduciary adviser or not.

23) Q. "I agree that annuities are not right for everyone but for some people they are a good option."

A. Good for whom? For people who to lock their money in prison in exchange for under performing a comparable low-risk portfolio of 75% bonds and 25% stocks and being taxed at a higher rate?

24) Q. "OK. Stocks are volatile. Bonds are slow and consistent. Then why not put 75% in bonds and 25% in an annuity?"

A. Because bonds and stocks work together! Stocks and bonds tend to balance each other out because money has to go somewhere, and when one outperforms the other you can percentage rebalance for increased returns. You cannot 'rebalance' and annuity! Your strategy to put 25% in an annuity would have backfired as recently as 2013 when stocks went up 33% and of course nicely balanced out a bond market that lagged 2%. To say that an annuity should be part of a portfolio is like saying that every football team should have a couple of bad players.

25) Q. "Indexed annuities are an excellent tool for baby boomers to get through retirement safe and secure."

A. This is nothing more than happy talk. It's a conclusion statement that is not backed by historical performance data to demonstrate that an age-appropriate bond/stock portfolio would put them at risk of running out of money or earning lower returns. In reality an annuity is an inferior "tool" that consistently robs seniors of their ROI (return on investment). An annuity is also an illiquid financial product that subjects investors to significant liquidity risk (because due to unexpected events approximately 25% or more of annuitants wind up having to withdrawal money before the surrender period and / or pre-age 59 1/2 penalty period has expired), higher taxes and risk of insurance company / state guarantee fund insolvency. The 2000's decade is a perfect example of how a simple portfolio of 75% AGG (total bond market) / and an ETF like VOO (the S & P 500 index) easily beat this index annuity.

26) Q. "Geoffrey VanderPal, Jack Marrion and David Babbel did a study on index annuities and concluded that they are a good choice for investors."

A. First of all, you conveniently cherry picked a supposed "study" that supports your job of selling annuities. Why have you skipped mentioning the other studies that completely contradict this study, such as those by by Craig J. McCann and William Reichenstein? Or what about the more recent study which found that index annuities returned an average of only 3.27%?

This Wharton School "study" reads like boilerplate insurance salesman talk. In fact according to this article people behind this "study" have what would appear to be glaring conflicts of interest. Babbel has consulted to the insurance industry. Marrion runs a web site and runs a service for the insurance industry, helping to promote the sales of EIAs! VanderPal was a broker / adviser. One has to wonder if he or his firm sold annuities. In other words, these guys do not appear to be the disintersted analysts that you would want heading up a study. But let's put this all aside anyway and examine this so-called "study" anyway.

They did not take a random sampling of insurance contracts from customers. What did they instead do? They apparently asked 27 insurance insurance companies to provide them with contracts. Of course, when left to select contracts of their own choosing, any insurance company would want to put their best foot forward! Who knows if all or any of the contracts were actual customer contracts? When Advisor Perspectives attempted to peer review the study, they were stonewalled by the authors of the study (who claimed confidentiality) and by all except one out of 27 insurance companies that participated. So this study is essentially useless.

Even if the contracts were real and random, Advisor Perspectives found the study to be flawed in many ways. You can read the article here.

Before reading the above adviserperspective response I noted that this "study" is fatally flawed in many ways:

1) This study states that the study is based upon "actual interest that was credited". It appears as though Babbel compared annuity annual interest payment "return" or "income base" with return on investment of a 50 / 50 portfolio. If so this is a case of comparing apples to oranges. ROI is the essential performance measure used to evaluate the efficiency of an investment or to compare the efficiency of a number of different investments, yet amazingly nowhere in this 16 -page report called "Real World Index Annuity Returns" is the term "return on investment" ever mentioned!!! It isn’t until the contract has ended when you cash out or die that you are able to calculate an actual ROI after all applicable fees and taxes are subtracted. This study also states that it did not account for surrender penalties, and it only evaluated 5-year time periods. Many index annuities have surrender penalties that stretch for 17 years. This study also did not mention whether these contracts had guaranteed income riders. According to some insiders, as many of 90% of annuitants choose this toxic guaranteed income rider. If so, that would quickly explain the high rates of fool's gold "return" claimed by this study. There's a big difference between "income base", "accumulation value" or "protected benefit value" and what matters most, namely return on investment. Confusing the basis for annual income payments with ROI is one of the top insurance industry deceptions.

2) The report also compared ultra-conservative (annuities) to moderately risky (a portfolio of 50% S & P stocks / 50% total bond index). It states that a 50/50 portfolio is a “proxy for broad market performance”. Nice slight of hand! The problem is that a 50/50 portfolio is not a proxy for assessing annuity performance versus normal conventional investments because it is not the lowest risk bond/stock allocation ratio. Yet from this flawed foundation, this study proceeds to jump to all sorts of happy conclusions about annuities. A proxy for assessing annuity performance is an alternative low-risk portfolio in the neighborhood of 28% stocks and 72% bonds. Roger G. Ibbotson who is the professor of finance at Yale School of Management determined that this was the lowest risk portfolio from 1970 until 2010.

3) Did the study compare annual rates of return based on compounded returns of both the 50/50 portfolio and the index annuity "returns" (apples to apples) or something else?

4) The study cherry picked a time period that conveniently ends at the worst possible year end point in recent years for stocks: January 1, 2008. So this is a worst case scenario study that favors annuities.

5) The study only looked at 5-year holding periods. What happened over the next 10 years of these contracts or however long the surrender periods were? Did the insurance companies lower caps as they are so famous for doing? Were there introductory "teaser rates"?

6) The study never implemented a simple rebalancing strategy for his 50/50 portfolio.

7) The study did not look at the higher taxes that annuitants must pay, which according to Wealth Manager more than offset the benefits of deferred taxation.

8)The study focuses on the risk of outliving one's money due to market volatility, without addressing the very real liquidity risk. It has been suggested that 25% of annuitants wind up pulling their money out early, and of course paying a surrender penalty. 25% is a very high risk!

Insurance companies do not give away money. They have overhead costs, their agents are paid usually between 5 and 20% of what you invest, and insurance companies must earn a profit too. So when anyone suggests that annuities are beating the market, this should sound the alarm bells. If it sounds too good to be true then it must too good to be true.

Great article that debunks the Wharton study.

27) Q. Who, coming off the decade of the 90s, would have been positioned in a "simple 75 bond / 25 stock portfolio"?

A. Who? A conservative investor who understands what an age-appropriate bond/stock mix is, and the same conservative investor who would consider an annuity. Again, anyone who lost their life savings from 2000 - 2008 made the critical mistake of taking on too much risk. It wasn’t the stock market’s fault. It wasn’t their fault for not putting their money in an annuity either. It was their fault for taking on too much risk, thinking they could time the market instead of adhering to an age-appropriate bond/stock mix. When someone tries to compare an annuity to something other than a low-risk bond/stock portfolio they are presenting a false choice.

28) Q. "Annuities are not for everyone, although they are a great tool for some.".

A. Not for everyone? That’s an understatement! According to Clark Howard "There's almost NEVER a circumstance when an annuity is called for." Ric Edelman, who is not even a fee-only adviser has said that out of some 16,000 clients he's only found about perhaps 10 clients who were a good fit for an annuity. Now would you describe 10 out of 16,000 “not for everyone" or “extremely rare"? You can bet that to Mr. Annuity Salesman “not for everyone" means just about everyone who steps foot in his office or comes to his "free dinner seminar"!

But by saying “not for everyone" it gives the false impression that annuity salesman have restraint and lines that they won’t cross even though annuities pay really fat commissions.

By the way the few people who are a good fit for an annuity are typically people who are vulnerable to civil lawsuits and they live in a state that protects retirement accounts from judgments. Remember OJ Simpson moving to Florida with his NFL pension? And only a lawyer can make that call. It is illegal for an insurance salesman to give legal advice (to buy an annuity to protect against judgements).

29) Q. You are biased because all you talk about are the negatives about annuities.

A. Who are you kidding? There is only one story to report about annuities: the truth. If the truth happens to be negative then negativity in and of itself is not "biased". If I were selling a commission-based product other than annuities, that might make me biased, but I don't. I don't sell anything. It's actually non-fiduciary advisers who are licensed to sell annuities who are not just biased but highly biased in favor of annuities. That's why consumers who visit this site are learning critical facts about annuities that their biased "adviser" never discussed with them.

30) Our firm specializes in wealth preservation.

Response: This is code for "Our goal is to sell you expensive insurance products that have guarantees because annuities and cash value life insurance products earn us the highest commissions at your expense". A fee-only (salary-based) fiduciary advisor does not "specialize" in low-risk, medium-risk or high risk strategies. They tailor whatever strategy fits the client.

31) Lambasting insurance agents for recommending annuities is like yelling at the Mexican restaurant owner for not selling Chinese food.

Response: The problem is that insurance agents don't tell the truth. They present themselves as "advisors" instead of what they really are -- Commission hungry salesmen who don't legally work for their customers and who have major conflicts of interest! Some financial planners are also licensed insurance salesmen. Customers think they will get unbiased money advice. Instead they get intentionally sold expensive financial products.

32) With inflation rising, now more than ever, you need an index annuity.

Response: Firstly, Mr. Annuity Salesman is falsely suggesting that the annuity will provide more income. You don't know that to be true because index annuities are private contracts. You cannot research past performance of index annuities. In reality, most annuities tease you with higher income initially, then fall by the wayside later in life. Secondly, inflation is an equal opportunity offender. It affects traditional investing money the same as it affects annuity money.

1 - 2 - 3 - 4 - 5 - 6 - 7 - 8 - 9 - FAQ - Top Annuity Lies

Note the misspelling of "advice". Use an "S" instead of a "C".

Disclaimer and Waiver - Nothing on this consumer advocate website is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy, hold or sell, or as an endorsement, of any company, security, fund, product or other offering. This website, its owners, affiliates, agents and / or contributors are not financial or investment advisors or broker / dealers and assume no liability whatsoever by your reliance on the information contained herein. The information should not be relied upon for purposes of transacting securities, assets, financial products or other investments. Your use of the information contained herein is at your own risk. The content is provided 'as is' and without warranties, either expressed or implied. This site does not promise or guarantee any income or particular result from your use of the information contained herein. It is your responsibility to evaluate any information, opinion, advice or other content contained. Always hire and consult with a professional regarding the evaluation of any specific information, opinion, or other content.