1 - 2 - 3 - 4 - 5 - 6 - 7 - 8 - 9 - FAQ - Top Annuity Lies

Index Annuities - Immediate Annuities

Immediate Annuities

Single Premium Immediate Annuities

Immediate Fixed Annuities

SPIA's

Longevity Annuities

Payout Annuities

SUMMARY: When you dump money into an immediate annuity you kiss your principal goodbye, you guarantee a diminished if not impoverished lifestyle for yourself later in life just when you might be most in need of increased income, the growth of your money stops once you start taking income payments, and therefore your heirs will receive zero ROI (return on investment) no matter how long you live. Typically by the time you reach your life expectancy there is no money left for heirs to inherit ("single life with cash refund" type policy). No roboadvisor recommends annuities.

"Dumping money into a SPIA is like deciding that taking a vacation at age 65 is more important than having food and shelter at age 85"

"Fee-only financial planners are not fans of annuities"

WHY IMMEDIATE ANNUITIES ARE A BAD DEAL:

- Immediate loss of your principal for life

- The growth of your money stops!

- Heirs get zero return on investment no matter how long you live

- Fixed annuity income payments don't keep pace with inflation

- A low-risk bond-heavy portfolio should eventually double what the annuity pays out

- The cost of living doubles about every 23 years

- Once you live to your life expectancy, heirs can expect no inheritance

Will your money last?

In retirement you are in a precarious position. Your money is working for you and so you don't want it to run out in the event that you live longer rather than shorter. For someone who has no heirs, in a perfect world you would gradually spend that money down, hitting zero on the day you die. Or if you have heirs that you care about, you would spend right down to a nice amount of money that you want to leave to your heirs.

Unfortunately we don't live in a perfect world.

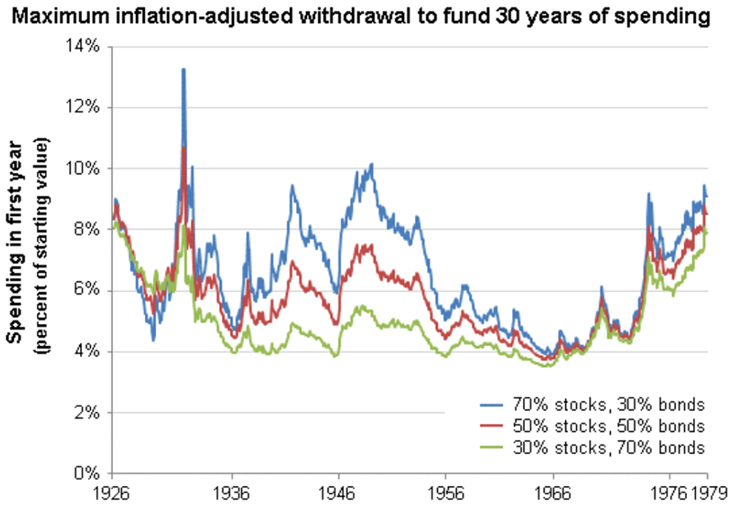

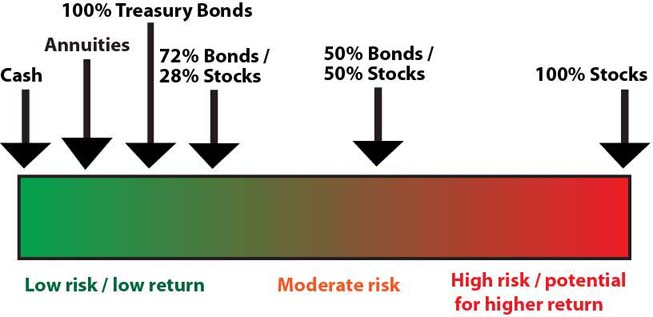

Today's 30 year old has a 30% chance of making it to their 90th birthday. Assuming that you might live into your 90's, you have to withdraw a reasonable amount per year. Otherwise your money may run dangerously low to the point that it is no longer producing enough income and may even run down to zero. As a rule of thumb you should be able to safely take out about 4% per year (AKA the "safe withdrawal rate") when you have a 30-year investing time horizon. Depending on what kind of returns are produced by bonds and stocks, you may be able to take out more or you may have to take out less. However the 4% rate assumes a general worst case market return scenario based on data going all the way back to 1926. There have been starting points after which you could have taken out as much as 8% without your portfolio of 30% stocks / 70% bonds dropping to zero. From 1970 to 2010 the lowest risk bond / stock allocation was 28% stocks (and 72% bonds) according to Ibbotson.

You should review your withdrawal rate once per year. Obviously taking out less is better because it will provide a cushion in case you have unexpected expenses and / or if the stock and bond markets under perform and / or if inflation runs higher than normal. The 4% withdrawal rate leaves room for your money to grow a little, thus keeping pace with inflation.

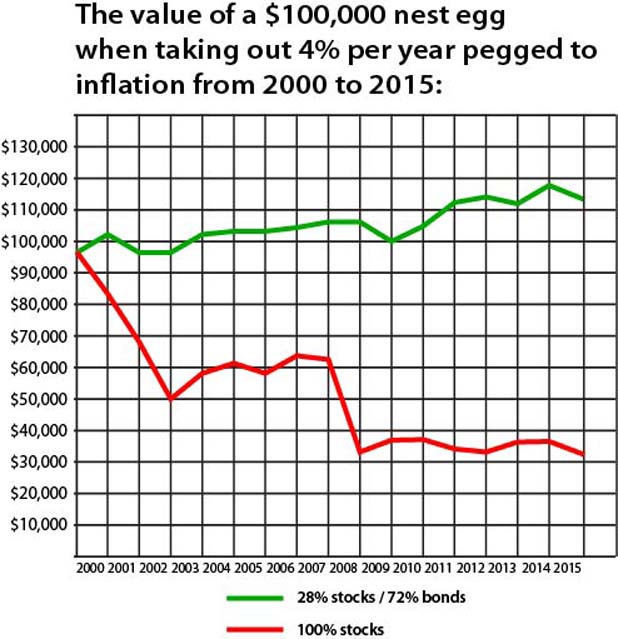

Above rate of withdrawal for each year: Jan 2000: $4,000, 2001: $4,136, 2002: $4,251.81, 2003: $4,319.84, 2004: $4,419.19, 2005: $4,538.51, 2006: $4,692.82, 2007: $4,842.99, 2008: $4,978.59, 2009: $5,167.78, 2010: $5,147.11, 2011: $5,229.46, 2012: $5,396.81, 2013: $5,510.14, 2014: $5,592.79, 2015: $5,682.28, 2016: $5,687.96

Note that the above chart assumes a worst case starting point of 2000. If we make 1998 our starting point we could have safely taken out 5% per year (not 4%) in order to maintain a healthy level of principal.

Sure I'll take 6% rather than 4%!

With an immediate annuity you are tantalized with the prospect of receiving more than 4%, such as with a "single life with cash refund" policy that pays 6% or more to a 65 year old male for as long as he lives (as analyzed further down this page). But is this a good deal when compared to what you could otherwise get by investing in a couple of stock and bond index funds?

Chances are that a licensed insurance salesman who calls himself by another title (such as "Certified Financial Planner") has suggested that you put money into an annuity, although an immediate annuity is probably last on his list of recommendations because immediate annuities "only" pay about a 3% - 4% commission. This is still more than the 0% he would earn if he instead recommended bond and stock index funds. So of course Mr. Adviser conveniently assumes, suggests or recommends that you should take income of 6% rather than income of 4%. He may do this by asking oversimplified leading questions like "would you rather live off of 4%, or would you rather get 6% or more?". Unfortunately it isn't this simple.

Before you run out and dump your money into a SPIA, you must understand that like anything good in life, accepting 6% instead of 4% comes at a price -- and potentially a steep price, particularly if the free markets perform up to historical averages or do better (you miss the boat even more), and also if you live long enough to see inflation dwarf that fixed 6% payment rate. If you die sooner than or right at about age 81 then your return on investment with a "single life with cash refund" policy can be expected to be to about zero. Ouch! No money left to your heirs or charity. Instead the insurance company inherits your money.

Back testing today's SPIA VS 1966 market returns

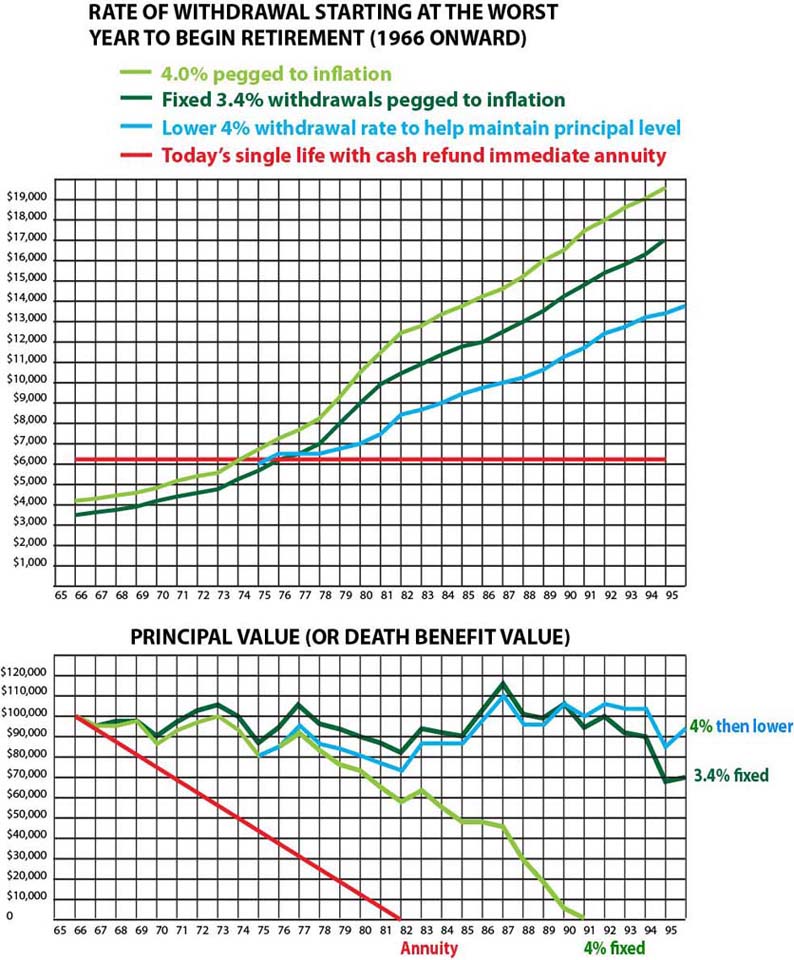

If ever there was a time when an immediate annuity would be expected to be a better deal, it would be starting in 1966. 1966 is regarded as the worst year to begin retirement because of low returns and rising inflation that reached as high as 13.5% in 1980. Unfortunately even if you retired in 1966, a SPIA bought today (paying 6.264%) would very quickly (age 74) start to pay below the 4% mark. Eventually you would be left in poverty with the annuity, earning an inflation adjusted equivalent of just 1.48% by age 90 and 1.27% by age 95. In this example we allocated 30% in the S&P 500 index and 70% in 10-year treasuries and calendar rebalanced on Jan 1 of every year using data from NYEDU. Withdrawals are pegged to inflation.

These were tough times and it was unavoidable. You only got to spend a consistent 3.4% per year. But at least you didn't find yourself trying to live off of 1.34% by age 95 with a SPIA. With a $100,000 investment if you put 30% in an S&P 500 index fund and 70% in T-bonds, then rebalanced annually you still had a $110,000 nest egg by age 90 and an $86,000 nest egg by age 95. By age 95, with a 3.4% rate of withdrawal, the 30/70 portfolio paid out $371,263.02 and still had a nest egg of $70,279.95. This compares with the immediate annuity which paid out only $197,700 and of course left zero inheritance by age 82. That's a grand total difference of $243,842.97. The immediate annuity got slaughtered!

Another alternative is to simply ease up on withdrawals as needed. The 4% rule should be evaluated on a yearly basis. So if your portfolio value starts to decline you can elect to reduce withdrawals. By easing up on withdrawals, our retiree had a nest egg of $107,536 by age 90 and $93,697 by age 95.

The lesson learned is that the 4% rule is an arbitrary line in the sand. You can reduce your annual spending if your principal starts to falter. Just because the 4% rule may start to "fail" at some point in time isn't the end of the world and most importantly doesn't mean that an annuity will perform any better over time. Yet annuity salesmen continue to use "the 4% may fail" headline as a red herring to bait unsuspecting investors into dumping their hard earned money into immediate annuities.

4% withdrawal rate can be increased to 5.1% - 5.5%

Starting retirement at age 75 or so? Very few insurance salesmen will tell you that once you get to just a 20-year time horizon (until death), the experts have said that you can take out between 5.1 and 5.5% (depending on which study you like) and not run out of money.

Inflation eventually dwarfs SPIA payments

If you think that taking out only 4% now is too little and depressing, try living on much less as inflation eats away at the purchasing power of those SPIA payments.

Assuming constant 3% inflation, SPIA payments of $6,590 at age 65 will seem like

$3,523 when you're 83 years old

$3,012 when you're 90 years old

$2,576 when you're 95 years old

Assuming constant 5.5% inflation, SPIA payments of $6,590 at age 65 will seem like

$2,258 when you're 85 years old

$1,728 when you're 90 years old

$1,322 when you're 95 years old

So the problem with immediate annuities is that they tease investors with too much income to start. Why is too much income a bad thing? Because that high annual payment rate stays fixed for life. Then later in life those fixed annuity payment amounts become too little due to inflation. History says that if you simply bite the bullet early in retirement by instead living off of the recommended 4% you will allow yourself cost-of-living increases every year and still be reasonably assured of not outliving your money. Eventually you should be able to take out more than the immediate annuity pays. Even in a worst case protracted stock market / recession scenario (analyzed further down this page) you surpassed the SPIA payment rate after about 23 years. And as previously mentioned, your heirs will enjoy a nice inheritance. In short, you can have your cake and eat it too as long as you eat sensible servings in the early years of your retirement.

Unfortunately some investors insist on wanting to take out considerably more than 4% in the early years of retirement. If you take out 6%, 6 1/2% or more from a traditional bond ETF / stock ETF portfolio, this increases the failure rate of a portfolio. You might run out of money before you die if the markets perform poorly like they did in the 2000's.

The best advice is to not insist on taking a high rate of return. Retire a little later or figure out a way to reduce your expenses and you should be rewarded in your later years of retirement just when you need that extra income most due to increasing medical and other expenses.

But if you absolutely cannot live on 4% then maybe an immediate annuity is right for you. Just understand that you will suffer in your later years due to inflation when those fixed annuity payment amounts lose purchasing power due to inflation. Think you will be spending less in retirement? Think again.

Also, as always, never let a non-fiduciary "adviser" (commission-based salesman) make this decision for you! Insurance salesmen are famous for asking simplistic leading questions like "would you rather earn 4% or earn 6.3%?" without explaining to you all of the negatives covered in this article, and without telling you that in reality you will only be earning between zero and about a 3% return on investment if you live long enough. Annuities pay large commissions to the sales agents who sell them, so never go to a commission-based adviser for any kind of money advice. If you need help then hire a fee-only fiduciary adviser on a one-time or one-task basis at napfa.org.

You cannot appreciate why immediate annuities are a bad deal unless and until you actually crunch the numbers based on historical returns of a low risk retiree portfolio of perhaps 67% bonds and the rest stocks. Beware of flawed studies that 1) include time periods going all the way back to the great depression when the markets were not adequately regulated, 2) assume that someone is taking out 6% in the early years, which is too much, 3) ignore the critical strategy of rebalancing, and 4) examine the failure rate of a risky portfolio (100% stocks or even 50% stocks) rather than a sensible retiree's 33/67 portfolio. From 1970 to 2010 the lowest rick allocation ratio was 28% stocks and 72% bonds. Any "adviser" who ignores this basic strategy of diversification is committing an act of pure deception.

From the perspective of annualized return on investment:

How would a 67/33 portfolio hold up through a

worst case scenario of 20+ years of recession?

We just looked at the importance of income for you the retiree. But from the perspective of your heirs, the most important measurement in comparing your investment options is annualized return on investment (ROI) or internal rate of return.

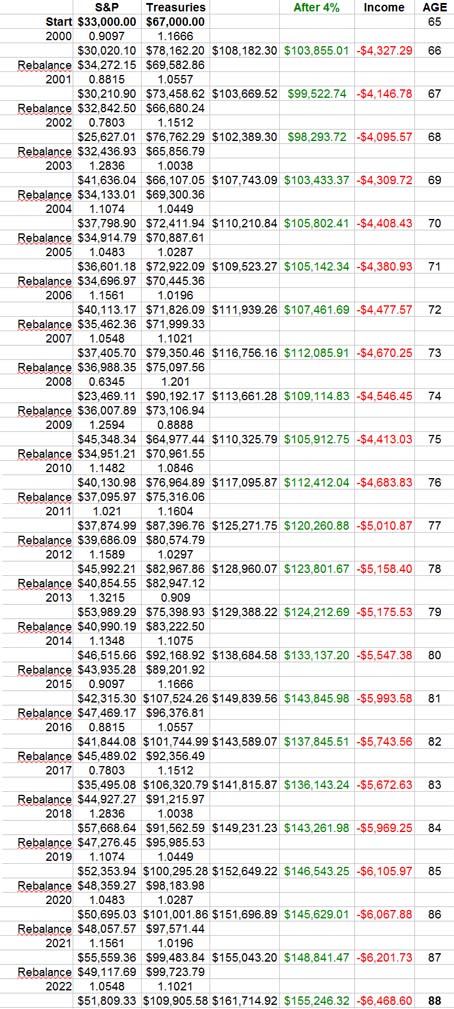

Let's compare what would happen if a 65 year old male put $100,000 into an immediate annuity versus what would happen if he invested 33% in an S&P 500 index fund and 67% in a total bond market index fund and took out 4% per year (according to the 4% rule), all assuming that we have a repeat of the "lost decade" bear market of the 2000's.

The best quote for a "single life with cash refund (premium refund)" policy that I found was 6.36% or $6,360 in fixed payments beginning on his 66th birthday. In the event that he dies sometime before all the premium (or initial investment amount) is paid back to him, then his heirs would receive the remainder, meaning the same $6,360 payments until the balance is fully paid back. That means that even if he lives to nearly age 81 then the return on investment of the $100,000 is zero because the insurance company is simply giving back the original money. If he lives to age 85 then his heir's return on his investment is just 1.3%. Assuming interest rates go up in the next 20 years then bank CD's may wind up performing better. Even if he lives to be age 100 his heir's return on his investment is still a paltry 3.4%. Keep in mind that only 0.0173% of Americans live to be 100. That's less than two 100th's of 1 percent.

Immediate Annuity return on investment if he lives to be....

65 - Zero return on investment

66 - Zero return on investment

67 - Zero return on investment

68 - Zero return on investment

69 - Zero return on investment

70 - Zero return on investment

71 - Zero return on investment

72 - Zero return on investment

73 - Zero return on investment

74 - Zero return on investment

75 - Zero return on investment

76 - Zero return on investment

77 - Zero return on investment

78 - Zero return on investment

79 - Zero return on investment

80 - Zero return on investment

~

85 - 1.3% return on investment

~

90 - 2.3% return on investment

~

95 - 3.0% return on investment

~

100 - 3.4% return on investment

Now let's see what would happen in a worst case scenario in which the 65 year old invested in a 33/67 portfolio at the worst possible time -- right before the 2000's bear market / recession began. And let's take it a step further. Let's assume that after 2014, we repeated the same 2000's bear market / recession all over again! How long would it take before his 4% withdrawals were equal to what he would be receiving with the immediate annuity? Sometime after age 87 his 4% withdrawals would surpass the fixed $6,360 immediate annuity payments AND he would have an extra $155,246 to his name! At this point he could safely take out more than $6,360 -- perhaps he could take out as much as $10,000 per year.

In all, the 33/67 portfolio paid out $117,757.25 over those 23 years and had $155,246.32 left to go to work producing future returns. That's a total of $273,003.57. This compares with the annuity which has only paid out $220,500 to this point. As always, the insurance company wins.

CLICK FOR LARGER VIEW:

Some immediate annuities have "inflation protection"

Unfortunately nothing in life is free. To give you increasing payments, the insurance company simply lowers the initial payment rate. So instead of giving you perhaps a fixed 6.5% payment rate, they'll start out with perhaps a 4.4% rate. Yes this is more than the recommended 4% safe withdrawal rate, but remember that the growth of your principal stops and your heirs will get zero return on investment. Whatever payments are given to you are subtracted from your principal which does not grow. Also often times there is a cap on the rate at which payments will increase. Don't expect your payment rate to keep pace with the 13.5% inflation like we had in 1980. So in reality you are only getting partial inflation protection coupled with zero growth of principal.

Mr Advisor has conflicts of interest

As with any insurance product, immediate annuities can only be sold by licensed insurance agents (or advisers or brokers who are also licensed insurance agents). These people stand to earn sizeable commissions if they manage to convince you to buy any annuity or other insurance product (universal life insurance, whole life insurance, etc). That is why you cannot base any money decisions on what Mr. advisor says. He is almost certainly a licensed insurance salesman. Hire a fee-only fiduciary adviser on a one-time or one-task basis when mulling over decisions on what to do with your money.

Final Thoughts

Later in life you may regret dumping money into that immediate annuity in order to take more money now in exchange for having less later. According to a survey by BankRate.com the number one regret of older Americans is not saving for retirement early enough. Number two was not saving enough for emergency expenses. Also on the list of regrets was not saving enough for your children's education and buying a bigger house than you can afford.

DISCLAIMER

KEEPING THINGS IN PERSPECTIVE: It should be noted that on this page we are examining very very low risk bond/stock allocations (example: 30/70) for comparison purposes. If someone is resigned to taking annuity-like risk (very low) on the very far left side of the risk / return spectrum then how does a similarly ultra-low risk allocation of bonds and stocks compare? That is what we are examining on this page. This is not to say that you the reader will want to take on this little risk. Allocation ratio should be carefully considered on an individual basis. Bob Brinker recommends a 50 / 50 allocation for the average retiree.

QUESTION: My 'adviser" says that some annuity riders and income options include COLA (Cost of Living Adjustment) or CPI-U (Consumer Price Index) annual increases for the life of the policy.

ANSWER: These are not free! The insurance company either charges large annual fees or they lower the income stream rates. Either way the insurance company will win and your returns will be mediocre.

Click here to read about most of the top insurance industry lies about annuities.